Developers and investors who move early may benefit most.

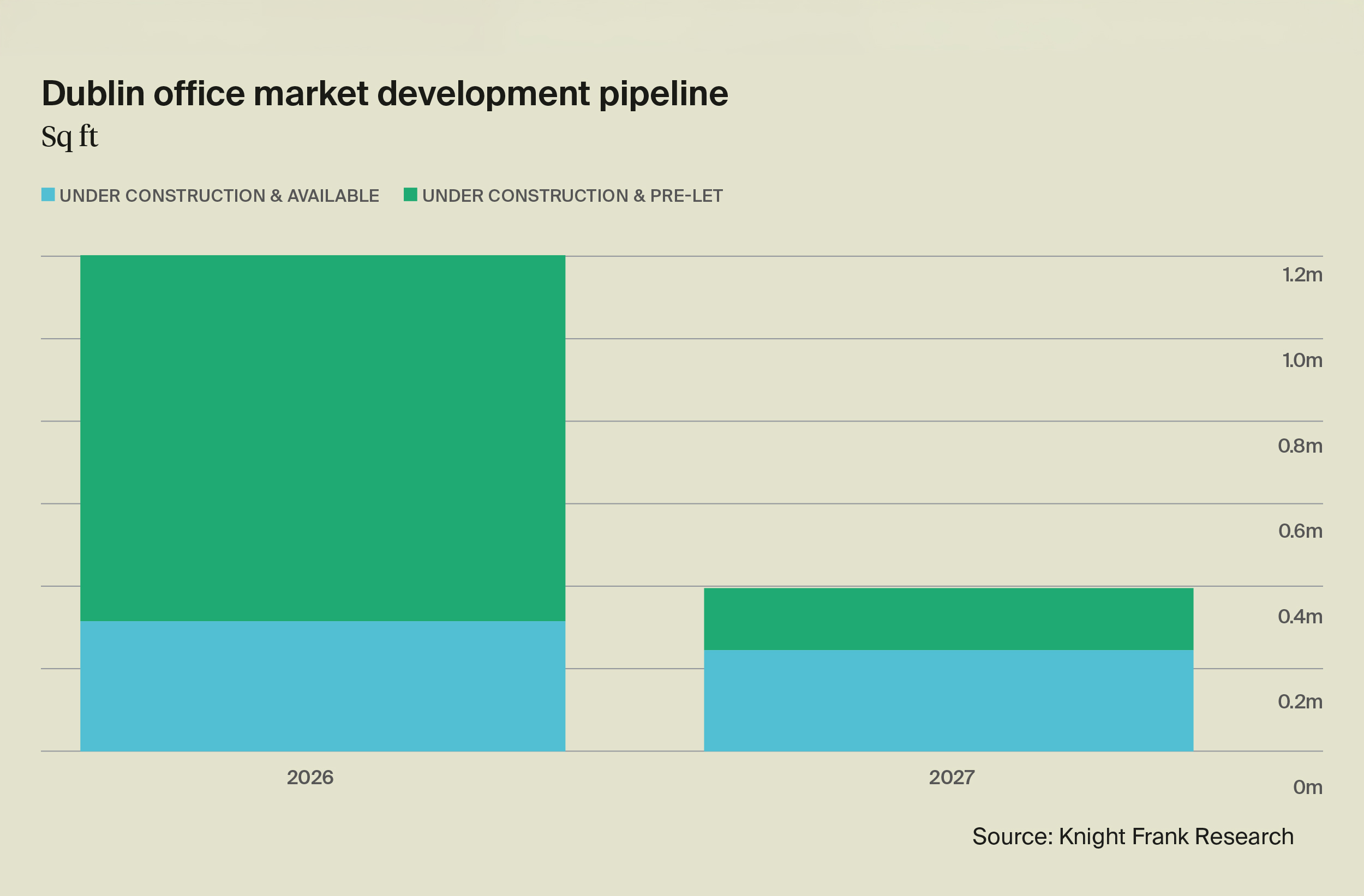

The most striking feature of Dublin’s office market today is the absence of future supply.

Approximately 1.0 million sq ft is due to complete across the remainder of 2026, with around 80% already pre-let. For 2027 completions, approximately 60% is already secured. Beyond this, there is no speculative office schemes currently under construction.

The absence of new starts is now the single biggest risk and opportunity in the Dublin office market. Developers and investors who move early would find themselves operating in a market with limited competing supply and increasingly favourable leasing dynamics.

Employment growth continues to underpin office demand

The labour market remains another important support mechanism for the office sector.

Projected employment growth of approximately 1.8% across 2027 and 2028 should continue to provide a reliable floor to occupational demand, particularly for well-located, office accommodation that also offers sustainable credentials.

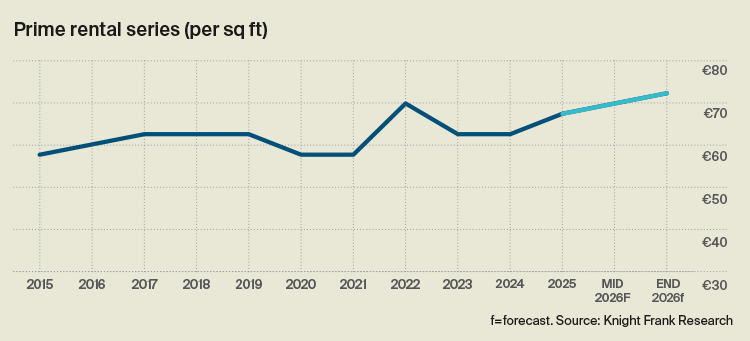

Rental growth

Prime rents remained stable during Q1 2026 at between €65 and €67.50 per sq ft.

However, with future supply becoming increasingly constrained, rental growth is expected to accelerate. Prime rents are forecast to reach €70 per sq ft during 2026, while pre-let transactions could achieve rents of up to €75 per sq ft.

Q1 2026 office market performance

The Irish economy entered 2026 from a position of strength, providing resilience despite renewed global volatility.

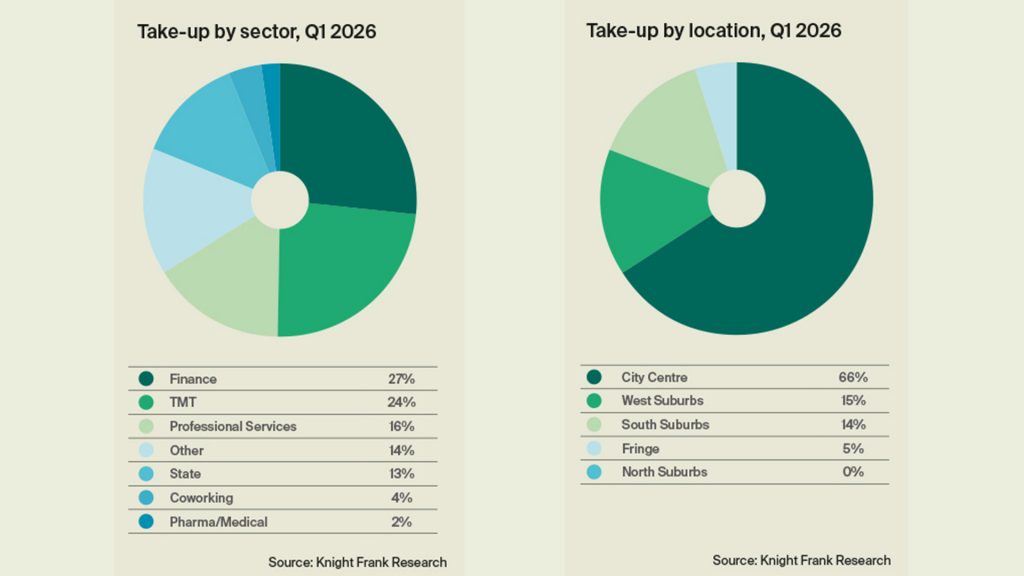

390,000 sq ft was transacted in Q1, broadly in line with Q1 2025 (406,000 sq ft), representing a solid underpinning of demand.

City centre locations continue to dominate, with increasing attention now shifting to Dublin 1 as Dublin 2 availability tightens.

TMT and Financial Services accounted for 51% of take-up, reinforcing the depth of demand from core occupier groups.

Total take-up for 2026 is forecast at 2.0 – 2.2 million sq ft, signalling sustained activity despite global headwinds.

Investment activity signals growing opportunity

While Q1 investment volumes were relatively modest at €443 million, this was heavily influenced by transaction timing, with a single large PRS transaction accounting for approximately half of total volume.

Encouragingly, a growing pipeline of larger lot sizes is expected to come to market throughout the year, particularly across both the office and living sectors including One Molesworth Street in Dublin 2 recently which recently sold for €110 million.

2026 will depend on how global geo-political events evolve and how any potential increases in interest rates impact global funding conditions.

Office market outlook supports development. Current pipeline activity does not.

The fundamentals of Dublin’s office market remain supportive. Demand is resilient, employment is growing, rents are forecast to increase, and occupier activity remains healthy.

To discuss the opportunity in greater detail, Joan Henry, Chief Economist & Director, Research can provide a comprehensive overview of the market fundamentals and outline why this development window is both real and increasingly time sensitive.

The findings form part of Knight Frank Ireland’s Dublin Office Market Report Q1 2026.

For further information, contact:

Joan Henry

Chief Economist & Director, Research.

Kevin Kavanagh

Marketing & PR Manager